5 FOMC members are scheduled to make 6 speeches this week, including Fed Chair Janet Yellen. How will the dollar dance along with their speeches?

The first non-farm payroll of 2017 fizzled out at 156K, market was expecting 175K jobs added. Unemployment rate rose slightly to 4.7% as expected, due to higher participation rate. Average hourly earnings came in at 0.4% versus forecast of 0.3%. Anyone who took a quick glance at these data would make a call to sell the dollar. Oh! … We forgot to mention the previous figure was revised upwards from 178K to 204K! I bet you would be scrambling to reverse your earlier decision to sell the dollar now. This is exactly what happened last Friday. The EUR/USD shot up 40 pips in an instant, only to reverse to wipe out the gain and went another 30 pips lower. All of these happened in the first minute after the data were released. The dollar remains resilient, as the data are not bad enough to derail Fed’s tightening plan.

5 FOMC members are scheduled to speak this week, including Fed chair Janet Yellen. We expect the speeches to echo optimism in Trump’s economy and also express concern of global uncertainties. It is just the start of the year, there is no necessity to steer away from their plan of 3 rate hikes, neither is there a hurry to raise interest rate soon. If the market does not see a high possibility of a rate hike in the first quarter, the dollar may weaken slightly this week.

UK PMIs scored a hat trick. All three PMIs came in better than expected.

- Manufacturing PMI : 56.1 vs 53.3

- Construction PMI : 54.2 vs 52.6

- Services PMI : 56.2 vs 54.8

However, the hat trick failed to inspire the sterling to maintain the lead for last week. It crumbled as possible “hard exit” continues to haunt the sterling and nothing is derailing the dollar from 3 rate hikes yet. We expect this phenomenon to continue, the sterling may rally on positive data, but will likely lose its gain thereafter.

The biggest event was PBOC’s intervention to prop up the yuan against dollar. Capital outflow, uncertainties in China’s economy and Fed’s tightening plan have resulted in the yuan coming close to break the 7.0 level, which has been maintaining a clean sheet for 8 years. The intervention strengthened the yuan by 1.3%, which also sent the offshore yuan (CNH) losing more than 1700 pips in 2 days, the biggest move since August 2015. PBOC has demonstrated time and again, they are ready to intervene whenever necessary. We could possibly see more of such interventions if Fed rate hikes bring the USD/CNH towards the 7.0 level again.

Our Picks

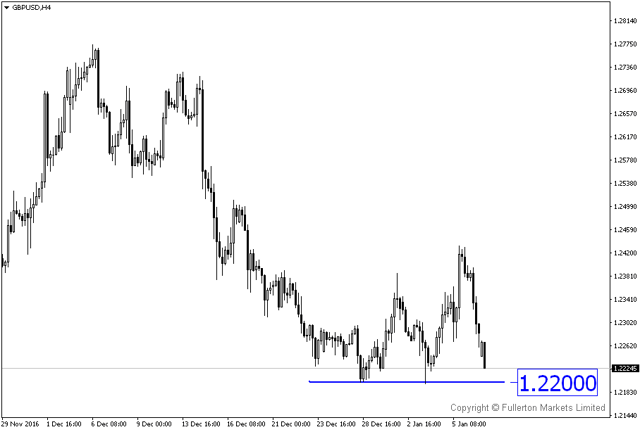

GBP/USD – Possible Long. Impact from the exit is unable to be assessed at the moment and Fed rate hike in near future is unlikely. We expect the 1.22 support to hold.

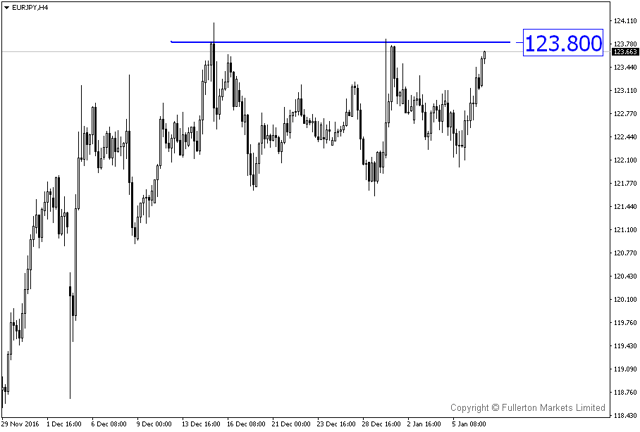

EUR/JPY – Possible Short. ECB stimulus continues and no further easing from BOJ. We expect the 123.80 resistance to hold.

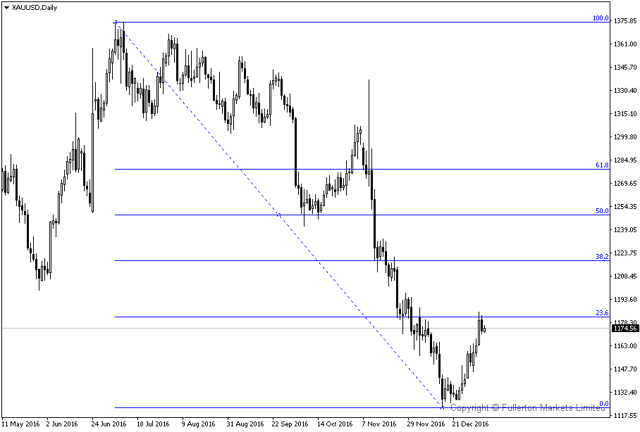

XAU/USD (Gold) – Possible Short. Gold is near 23.6 Fibo level, possible to look for short entry on prospect of Fed rate hikes.

Top News This Week (GMT+8 time zone)

Australia: Retail Sales m/m. Tuesday 10th January, 8.30am.

We expect figures to come in at 0.5% (previous figure was 0.5%).

UK: Manufacturing Production m/m. Wednesday 11th January, 5.30pm.

We expect figures to come in at 0.7% (previous figure was -0.9%).

US: Core Retail Sales m/m. Friday 13th January, 9.30pm.

We expect figures to come in at 0.5% (previous figure was 0.2%).

Fullerton Markets Research Team

Your Committed Trading Partner